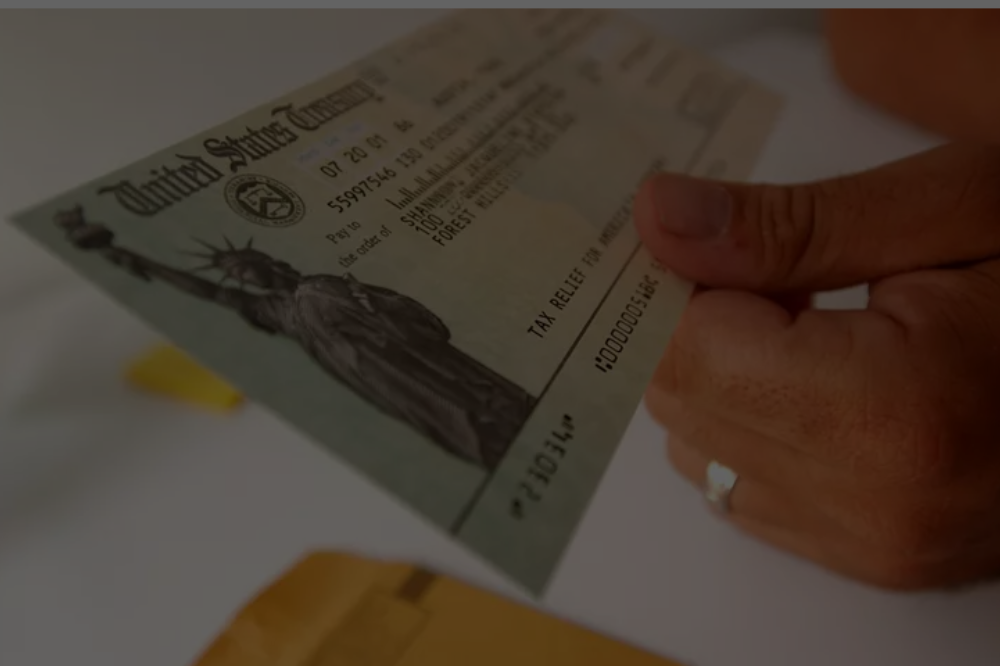

New York’s Inflation Refund? Rising prices have squeezed household budgets across America, but New York State is stepping up to provide some relief. The state is issuing inflation refund checks ranging from $150 to $400 to more than 8 million residents who qualify based on their 2023 tax filings.

These one-time payments represent the state’s effort to help residents cope with increased costs caused by inflation. The program automatically sends checks to eligible taxpayers without requiring additional paperwork or applications.

Understanding who qualifies, how much you’ll receive, and the best ways to use this money can help you make the most of this unexpected financial boost.

Who Qualifies for New York’s Inflation Refund

To receive an inflation refund check, you must meet three specific criteria based on your 2023 tax year:

Income Requirements: Your adjusted gross income must fall below certain thresholds. Single filers and those married filing separately need to have earned less than $150,000. Married couples filing jointly must have earned less than $300,000.

Tax Filing Status: You must have filed a 2023 residential state tax return in New York. This means you were a New York resident when you filed your taxes for the 2023 tax year.

Dependency Status: You cannot be claimed as a dependent on another person’s tax return. This requirement ensures the refunds go directly to taxpayers who file their own returns.

The state automatically reviews tax records to determine eligibility, so there’s no need to submit additional forms or applications if you meet these requirements.

How Much Money Will You Receive

The amount of your inflation refund depends on both your filing status and income level from 2023.

New York has structured the payments to provide larger amounts to lower-income households and those with more family members to support.

- Single Filers and Married Filing Separately: If you earned $75,000 or less, you’ll receive $200. Those who earned between $75,001 and $150,000 will get $150.

- Married Filing Jointly: Couples who earned $150,000 or less receive $400 per household. Those with income between $150,001 and $300,000 get $300.

- Head of Household: Single parents and others filing as head of household receive $200 if they earned $75,000 or less, or $150 if they earned between $75,001 and $300,000.

- Qualifying Surviving Spouse: This filing status receives $400 for household income of $150,000 or less, or $200 for income between $150,001 and $300,000.

The payment structure reflects New York’s approach to targeting relief toward middle and lower-income families who typically face the greatest burden from inflation.

When and How You’ll Receive Your Check

The New York State Department of Taxation and Finance began mailing checks at the end of September 2024. The process continues over several weeks as the state processes millions of payments.

Your check will arrive at the address associated with your most recently filed tax return. The state sends payments in batches, but not based on ZIP code or geographic region. This means your neighbors might receive their checks at different times.

If you’ve moved since filing your 2024 return or haven’t filed yet, you can update your address information through the New York State Department of Taxation and Finance website. This ensures your check reaches you at your current address.

The department cannot provide specific delivery schedules, and customer service representatives don’t have access to individual check status information.

Smart Ways to Use Your Inflation Refund

Receiving unexpected money presents an opportunity to improve your financial situation. The key is using it strategically rather than treating it as spending money.

Tackle High-Interest Debt First

Credit card debt should be your top priority if you’re carrying balances. With average credit card interest rates above 20%, this debt grows quickly and can overwhelm your finances.

Consider this example: A $2,000 credit card balance at 20% interest takes over 15 years to pay off with minimum payments of $53.33 monthly.

You’ll pay nearly $725 in interest charges alone. Applying a $400 inflation refund to this balance cuts the payoff time by two years and saves over $200 in interest.

Personal loans, payday loans, and other high-interest debts should also be prioritized. The guaranteed return from eliminating high-interest debt often exceeds what you’d earn from investments.

Build or Boost Your Emergency Fund

Financial experts recommend maintaining three to six months of expenses in an emergency fund. This money provides security during job loss, medical emergencies, or major unexpected expenses.

A high-yield savings account offers the best combination of safety and growth for emergency funds.

Some accounts still offer rates around 5% APY, though rates have decreased from their recent peaks. Even at lower rates, high-yield accounts significantly outperform traditional savings accounts.

Your inflation refund can serve as the foundation for an emergency fund if you don’t have one, or help you reach your target amount faster if you’re already building one.

Invest in Long-term Growth

If you’ve already paid off high-interest debt and built an adequate emergency fund, investing your refund can help build wealth over time. Consider these options:

-

- Retirement Accounts: Contributing to a 401(k), IRA, or Roth IRA provides tax advantages and compounds over time. Even small contributions can grow substantially over decades.

- Index Funds: Broad market index funds offer diversification and historically solid returns with minimal fees. They’re ideal for investors who want market exposure without picking individual stocks.

- Education Savings: 529 education savings plans offer tax advantages for future education expenses. Starting early gives investments more time to grow.

-

Make Strategic Purchases

- Sometimes spending money wisely can save more in the long run. Consider these strategic purchases:

- Energy Efficiency Improvements: LED light bulbs, weatherstripping, or programmable thermostats can reduce monthly utility bills.

- Preventive Maintenance: Car maintenance, home repairs, or health checkups can prevent more expensive problems later.

- Quality Items You Need: Replacing frequently broken items with higher-quality versions can save money over time.

Planning for Future Financial Challenges

While New York’s inflation refund provides immediate relief, it’s important to prepare for ongoing financial challenges. Inflation affects everyone differently, but having a plan helps you navigate future economic uncertainty.

- Track Your Spending: Understanding where your money goes each month helps identify areas where you can cut costs or optimize spending. Many free apps and tools make this easier than ever.

- Build Multiple Income Streams: Side hustles, freelance work, or passive income sources provide additional financial security. Even small amounts of extra income can make a significant difference over time.

- Stay Informed About Benefits: State and federal programs periodically offer assistance during economic challenges. Staying informed helps ensure you don’t miss opportunities for relief.

Maximizing Your Financial Recovery!

New York’s inflation refund checks provide welcome relief during challenging economic times, but their real value lies in how strategically you use them. Whether you’re paying down debt, building savings, or making smart investments, this money can serve as a stepping stone to better financial health.

The key is treating this refund as an opportunity rather than a windfall. By focusing on debt reduction, emergency savings, or strategic investments, you can turn this one-time payment into lasting financial benefits.

Remember that small financial improvements compound over time. The $400 you put toward credit card debt or into a high-yield savings account today can save or earn you much more in the future!